You’ve learned all you needed to know about financial security, you’re on a mission to achieve it, and you’re nailing it. Now you want to plan for the next stage: financial independence.

If this applies to you, congrats and welcome to this space that’s all about financial independence! We’ve put together insights, best practices, and ideas to get you started on your financial independence planning.

If you’re looking for ways to achieve financial freedom, Kudos to you! You’re well advanced and you’re probably familiar with what we’ll be discussing here. So be sure to check out this material written with financial freedom goals in mind: What is Financial Freedom?

Good. Now, all aspiring financially independent folks, gather up.

Before we get into the how of financial independence, let’s do a quick recap of what financial independence is and how it differs from financial security and financial freedom.

What is financial independence?

Sometimes mistaken for financial security or financial freedom, financial independence is actually a separate concept that is closely tied to the other two. In fact, it is the middle stage you can achieve in your financial journey.

While financial security is about having enough monthly income to cover your basic needs – food, house, clothing, utilities, transport, insurance, any debt or emergency expenses – financial independence is about having enough money to cover all of these basic needs, PLUS leisure activities, sports, travel, and anything else you want to include in your lifestyle.

And financial freedom is the ultimate stage you can reach in your financial journey, where you have enough money to cover your financial independence needs, AND ALSO be able to afford the lifestyle you desire, without having to work anymore if you don’t want to.

Why do you want to achieve financial independence?

As with financial security, it’s important to think or revisit your whys at this stage. Always think about your whys – live and breathe them.

Why do you want to achieve financial independence? Nailing down your whys will help you set up some clear financial independence goals. So clear, that you can visualize yourself achieving them.

When you’re thinking about your whys, make sure you and your life partner and family are on the same page. It’s the one thing that could make or break your entire journey – we’ll touch on this aspect later.

So once you’ve settled on your whys, you can start planning how to get where you want to get.

How to achieve financial independence?

This is where the fun starts. In what follows, we’ll synthetize best practices and advice from financial experts, as well as folks who’ve started their financial journey, and have already passed through the first two stages.

1. Set your financial independence goals

When it comes to reaching financial independence, or succeeding at any endeavor for that matter, your odds increase when you create a plan. And a plan starts with goals – which should be clear, measurable, and reasonable.

Starting from how we defined financial independence, identify and list all the things that you perceive as being part of a comfortable lifestyle you want to afford. Once listed, consider them your goals for this phase – your financial independence goals.

But keep in mind that these new goals do not replace the ongoing, short-term and long-term goals that you’ve set for yourself in the financial security stage – you need to keep funding your short-term and long-term goal fund, as well as your emergency fund!

What this means is that you’ll need to add some new entries to your balance sheet that account for potential expenses associated with these new goals.

2. Start from a sound premise: high income is not wealth

Many people think that having a high income makes you wealthy enough to retire rich. But that is a myth. Some people earn fabulous incomes during their lifetimes, and still retire poor. Others have to make do with much lower incomes throughout their lives, and yet retire multi-millionaires.

How is that even possible, you ask? It all comes down to spending habits: Some prefer to spend their income the minute they earn it on things they don’t really need, others choose to spend only as much as they need to cover their most basic needs and invest the rest to accumulate wealth.

Now, it would be unrealistic to say that you could accumulate wealth with a small income. You probably could – but that would take years and years. So if you’re currently relying on a small income, think of how you could create some extra sources of income. This way, you’ll be able to accumulate more wealth faster – if you’re clear about your goals and you practice healthy spending habits! However, “faster” does not mean tomorrow or next week. Accumulating wealth is a slow process that takes time and commitment. Keep this thought present, always!

3. Create extra income to invest

We’ve touched on this topic a little bit when we talked about financial security – how finding other sources of income can help achieve your financial security goals faster. Here we’ll touch upon what type of income sources would best benefit you at this stage and you’ll see why.

First, let’s look at the types of income streams you could work to develop. One the one hand, there’s the earned income – money you earn by getting actively involved in an activity. This could be a job, where you’re working for someone else, or self-employment. On the other hand, there’s the passive income – money you earn without having to be actively involved in an activity.

When it comes to developing extra sources of income, most people think of earned income: Taking on additional jobs, starting their own business, buying and selling things for profit, etc. Passive income from rentals, the stock market, or any other source that at one point starts generating money without your involvement, is not necessarily top of mind – because it is not as “tangible” or it involves some prerequisites that many lack, such as owning a property for renting purposes, or having the resources needed for an initial investment.

Now, you don’t have to opt exclusively for either an additional earned or a passive income source. You could add an additional earned income source and also consider a passive one at the same time. Or just consider an additional passive one.

Adding a passive income source is, in fact, a best practice and you can learn more about the reasons to do so in books like The 4-Hour Workweek. But essentially, it all comes down to time. Earned income requires more of your time. You are basically trading your time for money. Time that you could otherwise spend with your family, enjoying life. With passive income, once you’ve set the source up, it will only require some maintenance from time to time, but a great deal less than what you’d allocate to an additional source of earned income.

Ideas for sources of passive income abound, but here are a few popular ones to get your groove on:

- Rentals

- Interest-based / bonds

- Stock market shares / Index funds / dividends

- Capital gains

- Royalties from letting others use your creations, i.e. designs, photography, processes, ideas, etc.

4. Create a portfolio of assets

Okay. You’ve reached the point where your income covers your basic expenses and allows you to save and invest. Now it’s time to build your asset portfolio.

Why do you need one? Short answer: Risk reduction. Long(er) answer: If you spread your investment money throughout several assets, when one suffers from a market downfall, another may make up for the loss. So a portfolio of assets helps you reduce the risk of losing all your money, all at once.

Now, what type of assets should you include in your portfolio? The more diverse you make it, the better. How much should each asset represent of your overall portfolio? That’s really a personal decision that should be based on your age, goals, and your risk tolerance.

For example, if you’re in your thirties, have a higher risk tolerance, and you’re looking for higher returns in a short period of time, investing more in stocks may make more sense for you.

There are several asset allocation models out there that cater to different ages, goals, and risk tolerance levels – tried and tested by financial experts. Here are some examples:

- Conservative Income Portfolio

- Growth Portfolio

- Ray Dalio All Weather

If you’re just starting to build your portfolio, you may want to use one of these examples in the beginning. If you’ve already built it, these examples may inspire you to make some changes. Either way, check them out!

5. Get to know your taxes

If you’re looking to build an asset portfolio, one piece of advice you’ll hear repeatedly is: Make sure it’s tax-efficient!

Regardless of where in the world you reside, you will have to pay taxes for the revenue your assets generate. Taxes differ from asset class to asset class, and the level of taxation per asset class differs from country to country.

When building an asset portfolio, you need to be mindful of the taxes imposed by each asset class you’re considering, per the tax laws in your country. For example, taxes on gains derived from certain assets could be so high that your gains after paying those taxes would amount to just a meager sum; in this case, you may want to think twice about whether you’d be willing to leave that much money on the table. Your local government may offer some incentives for certain types of assets, such as deductible contributions or tax exemptions; in this case, you may want to consider including those in your portfolio.

So do your research or get proper advice from a local tax consultant before diving into investment decisions.

6. Focus on compounding

Any Warren Buffet fans in the audience? Well, then you know what this segment is about. Everyone recognizes the powerful force that is compounding. In fact, it’s one of the basic principles of financial independence.

Okay, now that you have decided on a portfolio of assets, keep in mind that each of those assets can generate exponential gains, if you apply the principle of compounding.

For example, let’s say that your asset portfolio currently consists of stocks, bonds, real estate properties, and deposits. When you start reinvesting the gains from these assets – dividends, interest, capital gains, etc. –, and they start producing their own gains, that’s when compounding takes place. Your investment money start growing at an accelerating rate, and you experience the compounding snowball effect.

Let’s take another example to see just how powerful this snowball effect can be. Say you have $1000 put aside and you want to invest it in S&P 500 stocks. Let’s see what gains this investment can yield in 10 years’ time in a couple of scenarios:

A. When you only make the initial $1000 investment;

B. When you make the initial $1000 investment, and additional monthly contributions.

Step 1. Use any compound interest calculator such as the one provided by investor.gov to calculate the estimated value of the initial investment in each scenario.

Step 2. With any calculator we need either an interest rate or an estimated average return rate of the investment, to get an idea of how it will perform in the future. The average annual return of the S&P 500 index is 10% and we’ll use this number in our calculations.

Step 3. Fill out the calculator fields and hit calculate:

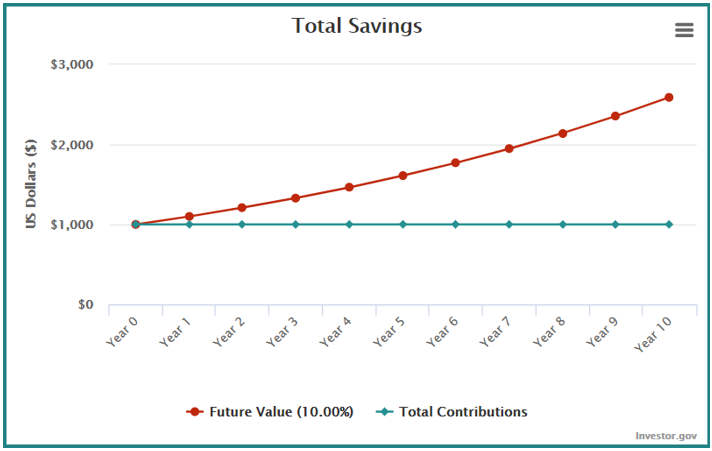

Scenario A:

The inputs to the calculator selected at Step 2. are:

- Initial investment: $1000

- Monthly contribution: 0

- Length of time in years, or the investment period: 10

- Estimated interest rate – here we’ll use the average annual return rate from Step 2: 10% average

- Interest variance range: 0, because we’re using the average annual return

- Compound frequency: annually.

And the result: If you invest now $1000, in 10 years, you will have $2,593.74.

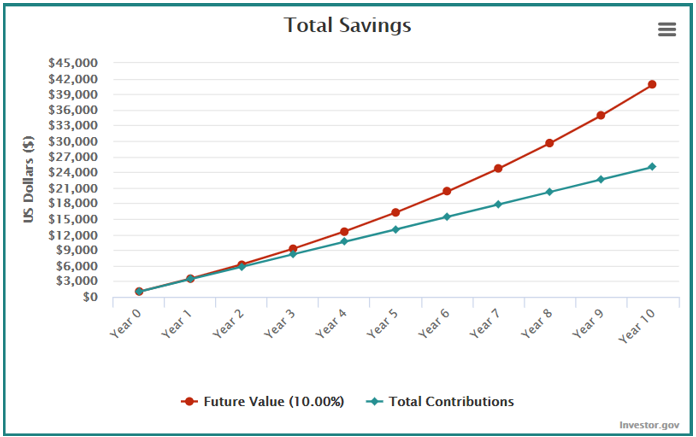

Scenario B:

- Initial investment: $1000

- Monthly contribution: $200

- Length of time in years, or the investment period: 10

- Estimated interest rate – here we’ll use the average annual return rate from Step 2: 10% average

- Interest variance range: 0, because we’re using the average annual return

- Compound frequency: annually.

And the result: If you invest now $1000 and make additional monthly contributions of $200, in 10 years, you will have $40,843.56.

Gaining more than double on your initial investment (Scenario A) in 10 years is great, isn’t it? Growing it by more than 40 times (Scenario B) is impressive! And just imagine the possibilities. If you’re just starting out, you can play with whatever calculator you find to test various scenarios. This will help you internalize the power of compounding and get you focused on it.

With HitFinancialFreedom, you can test comprehensive, real-life scenarios for accurate results that are based on your actual portfolio and asset performance over time. Check it out here.

7. Choose your FIRE style

Financial Independence / Retire Early or FIRE is the popular financial movement everyone talks about, but few succeed at keeping up with it.

FIRE was born from the Your Money or Your Life book published in 1992, and promotes frugality or drastic expense cuts, extreme savings, and heavy investments. These practices put you on an accelerated path to financial independence: There are people who achieved financial independence by saving up to 70% of their annual income over periods of 10 years or less – some in their twenties! Let’s call this the “rapid” FIRE approach.

However, saving up to 70% of your income is no easy feat. It requires living on a low budget and forming frugal habits. When deciding what percentage of your income you’re willing to save and invest, run some expense-savings scenarios. Choose the one you’re most comfortable with, but don’t compromise on anything that is crucial to you living a good, healthy life.

Now, if you’re not comfortable with a frugal lifestyle, you have to find an approach that feels right to you. Many people choose to take a “slow” FIRE approach, where they practice moderate expenses and savings. If you go this route, you just have to accept the fact that will take a bit longer to reach financial independence.

If this whole FIRE approach sounds a bit daunting, you may want to start with a small change in your purchasing habits: choose the enough-to-get-the-job-done over the I-can-afford-more-than-what-I-need.

Say you’re looking to buy a car to drive from point A to point B and you’re faced with two options:

1. You could buy a new car, because you can afford it;

2. You could buy a used car, half the price of a new one and still in good condition to serve the same purpose.

If you have a tendency to choose what you can afford, then your choice will result in a much lower savings rate than if you went for the enough-to-get-the-job-done option. In fact, by always going with the “afford” option you may never be able to save enough and reach financial independence. Just some food for thought.

8. Make sure you and your life partner are on the same page

The one thing that could make or break your entire journey is you and your life partner not working toward the same goals.

It’s important that you both sit down and discuss your vision for the future – individually and together, your whys, your non-negotiables, and the things each of you are willing to compromise on to reach consensus.

Make sure that the path you choose works for both of you, so you both embark on the journey with the same level of excitement and motivation. Because financial independence can be a difficult journey, with risks and ups and downs. And you both need to be clear on what you’re getting yourselves into and why. When things get difficult, you’ll both need to remember your whys. When one is down, the other will need to show their support and resurface the whys. When things go well, you’ll both share the excitement, and motivate each other even more.

If you are not on the same page with your partner, their lack of commitment and support, and potential disbelief may end up – willingly or unwillingly – sabotaging your efforts.

9. Teach what you practice to relatives

When embarking on this journey, it’s also very important that you have supportive family and friends. You may decide, for example, that it would be better for your financial independence goals to move to a city with lower living costs. If your family starts questioning your decision, you’ll all feel disappointed with one another. And this will only make your journey more difficult. So make sure they know about your goals and your whys and encourage them to take a similar approach to their finances. This will help them understand you better and gain some benefits of their own in the long term.

Now, imagine yourself in ten years’ time: financially independent or even financially free, affording the life you always wanted and worked hard to get. Undoubtedly, you will also be able to help relatives in need. And you will. But what if they come back to you for help over and over again? Will you fuel their dependence on you? At what cost? In such cases, you will need to help them become financially secure or even independent themselves. Share from your experience and guide them. You’ll both benefit from the experience.

And one last point: If you have kids, make sure you teach them everything you know about financial independence. Get them involved to contribute to your common journey. The knowledge they;ll gain along the way will help them start their adult lives as already financially independent people.

10. Take care of your body and mind

Last, but not least, put your physical and mental health first throughout the journey. Because, when you’re healthy, you can do anything – you are able to focus 100% on your goals. Any other worry or concern takes away from that focus.

Exercise. Meditate. Create a morning routine and stick to it. Practice mindfulness – eat mindfully, walk mindfully, breathe mindfully. Engage all your five senses frequently in outdoor activities – clear your mind, disconnect, and charge your batteries when you’re feeling low on energy.

On your journey to financial independence you will encounter risks, stress, disappointment, and many ups and downs – quite a bumpy road! But because you are working on achieving your dreams, you’ll also get a sense of purpose, meaning, and fulfillment.

So hang on tight and enjoy the ride!